Sector: Banking

A Quick Snapshot of Bandhan Bank

When I hear the name Bandhan Bank, one word comes to mind—“Micro Loans.” And rightly so, because the bank’s roots are deeply tied to the microfinance space.

It all began in 2001, when an NGO called Bandhan Konnagar was set up to support underserved women in West Bengal. Later, in 2009, this NGO spun off its microfinance business, which evolved into what we know today as Bandhan Bank.

As of Dec 2024, the bank’s loan book stands at ₹1.32 lakh crore.

Breakup:

- 42.5% – Micro Loans (Emerging Entrepreneurs Business + Agri + Small Businesses)

- 26.1% – Commercial Banking

- 24.7% – Housing Loans

- 6.7% – Retail Loans

Key insight: The micro loan share has come down from 87% in 2018 to 42.5% in 2024—a deliberate and healthy shift in my view.

Why Micro Loans Are Risky

Micro loans, while impactful, come with elevated risks:

- GST disrupted many small/micro businesses.

- Demonetisation nearly wiped out informal cash-based operations.

- COVID caused major delinquencies in repayments.

- These loans tend to have higher NPAs than secured or retail lending.

When economic turbulence hits, microloans are the first to suffer—and Bandhan Bank paid the price. The stock, once at ₹700 levels in 2018, has been in a consistent downtrend since.

This context isn’t to scare you—it’s to highlight the risk-reward nature of micro lending.

Financial Health Check

Bandhan Bank was highly profitable pre-COVID (₹3,000 crore PAT in 2020), but its earnings have since turned volatile.

For example:

- Dec 2023 PAT: ₹733 crore

- Mar 2024 PAT: ₹55 crore

A shocking 90% drop, largely due to aggressive ₹3,850 crore debt write-offs in Q4 FY24.

Their GNPA was around 7% in 2023 and is now down to ~4%—thanks to these write-offs. The biggest challenge has been cleaning up their bad loans and pivoting towards secured lending.

FY25 Performance Snapshot (as of Dec 2024)

- Deposits: ₹1.41 lakh crore (+20% YoY)

- Gross Advances: ₹1.32 lakh crore (+14% YoY)

- Secured Advances: +34% YoY; now ~50% of total loans

- GNPA: 4.7% vs 7.0% YoY

- Net NPA: 1.3% vs 2.2% YoY

- 9M FY25 PAT: ₹2,427 crore (+12% YoY)

- Q3 FY25 PAT: ₹426 crore (-41.8% QoQ)

If we set aside Q3 hiccups, this is a decent recovery considering the tough liquidity conditions until early 2025.

Tailwinds: RBI’s Surprise Relief for Micro Lending

On Feb 25, 2025, RBI gave major relief to unsecured lenders:

- Risk weight on loans to NBFCs reduced from 125% to 100%.

- Consumer loans also saw risk weights drop from 125% to 100%.

These changes ease capital requirements, making micro lending less punitive. This policy shift gives Bandhan Bank a breather and could improve sentiment around the stock.

Leadership Transition & Clean-Up

Founder MD & CEO Chandra Shekhar Ghosh retired in July 2024. Around the same time, the CTO and Chief Audit Director also exited—sparking market rumors, especially after a NCGTC audit flagged concerns about fake customers and fraudulent insurance claims.

However, BB cleared the audit and was not found guilty.

The RBI then approved Mr. Partha Pratim Sengupta—a veteran banker with 40 years of experience and former MD & CEO of Indian Overseas Bank—as the new CEO. He’s now overseeing a transformation agenda.

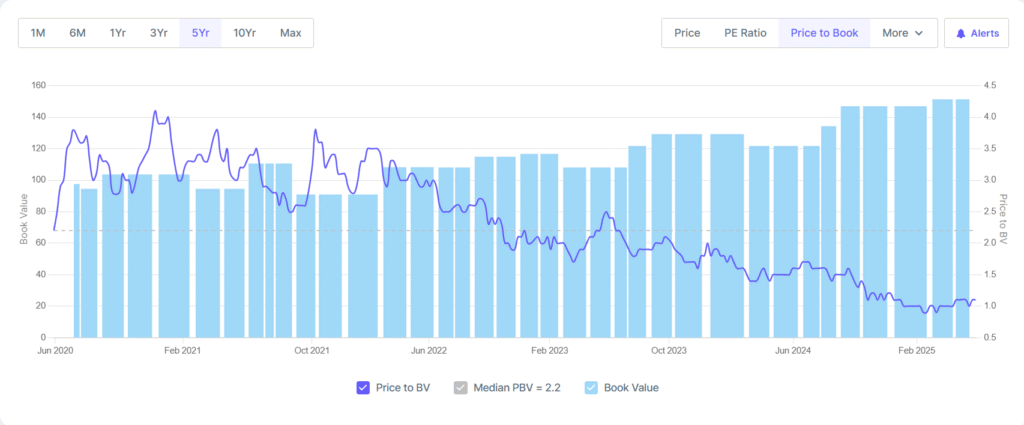

Valuation Check

- P/E Ratio: 9.72 vs industry average of 10.98

- P/B Ratio: 1.02 vs industry average of 1.14

Historically, this is Bandhan Bank’s lowest ever P/B, signaling potential value.

Between Apr–Oct 2024, the stock was consolidating in the ₹160–200 range but fell further—likely dragged by the broader small-cap sell-off.

- Promoters: Steady at ~40%

- FIIs: Down from 28% (Jun) to 23% (Dec)—consistent selling

- DIIs: Stable at ~15%

Final Thoughts

- The bank has had quality concerns in the past.

- Leadership change brings uncertainty but also fresh vision.

- Valuations appear reasonable.

- This may be a long-term play that needs patience (1–2 years).

- Question remains: Why choose BB over stronger players like HDFC, ICICI, or Axis?

Disclaimer: I am NOT a SEBI-registered advisor. This content is for educational purposes only and not a buy/sell recommendation.